Top-Rated Health Insurance Companies in America: Full Comparison of Plans and Costs

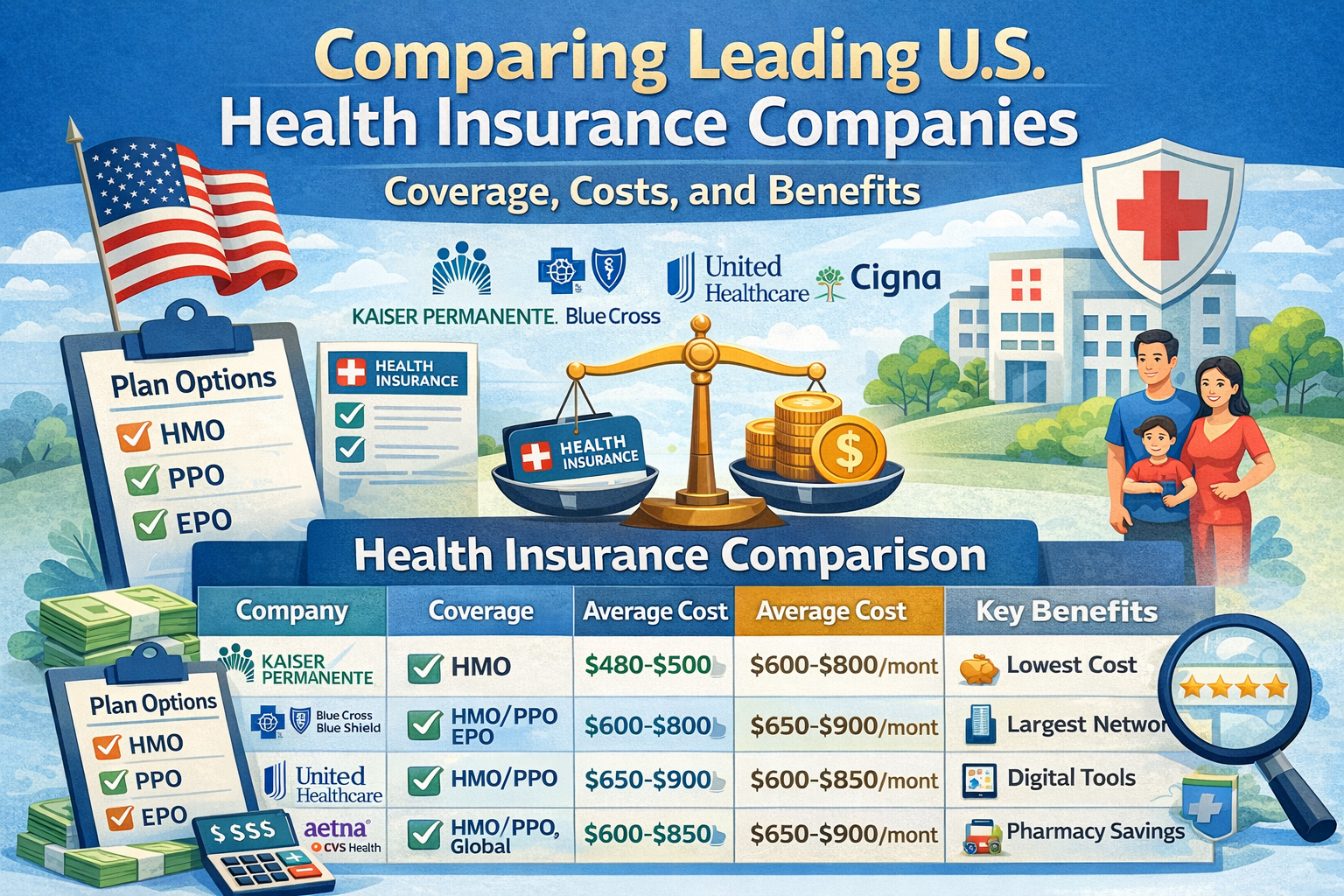

The ranking of top-rated health insurance companies in the United States is determined through a combination of measurable variables including customer satisfaction, financial stability, claims processing efficiency, provider network size, cost structure, and the breadth of benefits offered across plan tiers, and within this framework, a consistent group of insurers—Kaiser Permanente, UnitedHealthcare, Blue Cross Blue … Read more